Combating Insurance Misselling with AI

At some point of your life, you may have been approached by your bank's Relationship Manager, a friend, or even a relative - and promised very high, secure returns on 'investments'. You know, the ones that seem too good to be true? They would present a neat, shiny Excel sheet with calculations assuming high growth rates - and the maturity returns would seem baffling. Only to later (could be a week, a month, or years!) realize that they were trying to shove an insurance product for their own target's sake.

Insurance mis-selling is a grave travesty of consumer rights. In India, particularly, the problem has become so rampant that even the regulatory body - IRDAI - has started to take note of it. In its Annual Report 2024-25, grievances categorized under 'unfair business practices' rose to 26,667 in FY25, from 23,335 in FY24, an increase of about 14% year on year. But how does it affect the wider society?

The Targets Trap

At a fundamental level, misselling happens where a customer is convinced to purchase policies and pay hefty premiums for them, when they actually have an entirely different financial need. What has exacerbated the problem is driving national financial inclusion schemes - such as the Jan Dhan scheme, where everyone gets a bank account for them - without an adequate emphasis on the corresponding financial literacy and awareness levels. Due to perverse incentive structures, banks and their agents prey on unaware customers who place their trust on these institutions - in turn making a good cut for themselves from high commission rates that these products offer.

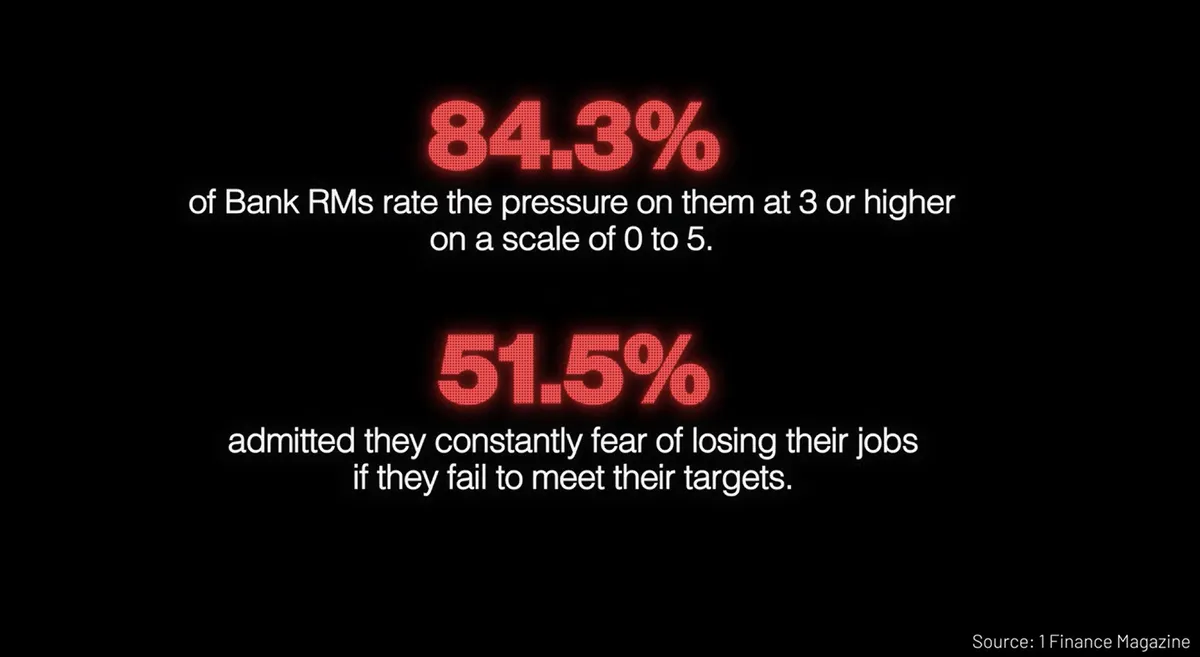

It has also been observed that these agents themselves are not intricately aware of the policy details. They are also constantly looking at the end of a barrel if they are not able to meet their sales targets. Look at the numbers from a documentary (linked below):

My personal regimen is to segregate term insurances from investment products. I do not treat the umbrella insurance cover that I have for my life as an investment decision. Conversely, I would not expect investment products to offer me life insurance. Mixing the two often results in a suboptimal product that neither provides sufficient life coverage, or a decent Internal Rate of Return.

There's an excellent documentary available on the internet that revolves around this plague and has real conversations with victims of such policies. I'd highly recommend it to anyone - it is only an hour long, but this video is one of reasons that IRDAI has recently stepped-up vigil.

Utilizing AI to Cut through the Noise

This is where the Artificial Intelligence boom can really help combat the vice of mis-selling. If you really think about WHY these agents can get away making false claims, you'd understand that it happens because of the verbosity of the policies themselves. Any endowment policy, or for that matter Unit-Linked Insurance Policy (ULIPs), comes with a monstrous set of Terms & Conditions, often running into tens of thousands of words, and fifty-plus pages of caveats.

One cannot pragmatically expect to read through and understand every single line of such a document. It is simply beyond what humans are made for. And that is our cue - if it's not something that we enjoy doing, AI for sure excels at. The entire growth trajectory of popular GPT models such as Gemini, OpenAI, Anthropic and their likes have risen from their ability to parse massive documents and extract meaning from them.

One of my relatives had recently approached me to review a policy document with one of the Indian private insurers. There are in their sixties and were sold four policies worth some lakhs cumulatively. The premiums would continue for 10-12 years, with guaranteed pension amounts. What they weren't told was that the maturity benefits only accrue at the 30 and 40-year from the policy inception. This was crazy, because the policyholder would be almost a hundred years by the time they would get the entire maturity benefits back. Planning for the future is one thing; locking all money till 100 years is quite another.

I started my analysis by extracting the policy brochure from the internet and uploading it to Gemini, Google's premier AI model. Usually, I look for a key terms understanding as a layman would prefer. Zero fluff.

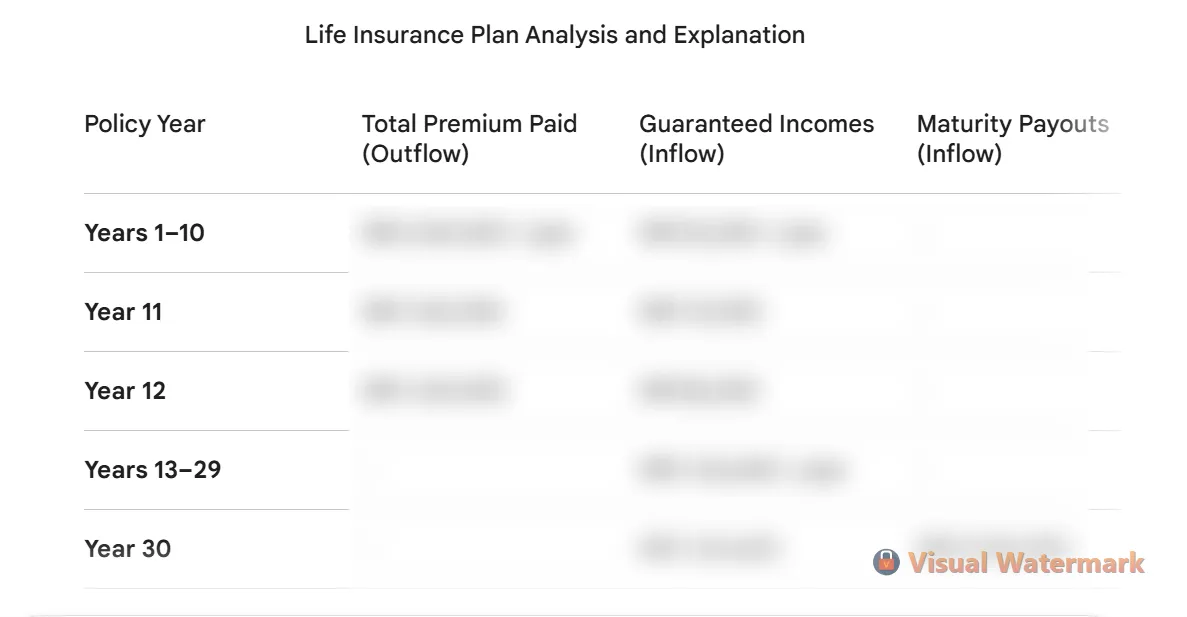

It explained, in a point-wise summary, the essential nuances. This is where I caught the first red flag that the policy was essentially a forty-year lock-in scheme disguised as a pension plan. To dig deeper, I then prompt the tool to generate the yearly payments made, versus the annual returns, and the maturity calculations. It is able to formulate all of these details in an exceptionally structured manner, making it very easy to interpret. It also comes back with IRR calculations, suggesting that in the long run, the policy would generate around ~5.5% yearly, which is standard for such policies.

Since the policy was ultimately ineffective and against the wishes of the policyholder, we were able to draft a notice for cancellation under IRDAI's free-look period mandate of 30 days since the start of policy. Again, Gemini was able to create a well-rounded application citing relevant legal provisions and the scheme's own fine prints, which was ultimately submitted to the insurance company.

If you're further curious about the nitty-gritties of the brochure, you can keep questioning the Large Language Model and it will happily oblige. This is where AI gets democratized and actually empowers ordinary citizens to not fall into the trap of verbosity alone while making financial decisions. While I have Google's AI plan subscription, most of the leading companies offer generous free-tier limits that should more than suffice for essential analysis and dissection of the policy documents.

Takeaways and Suggestions

If you are reading this piece, I know that you are amongst the better placed in society. Yet we have hundreds of thousands of people who are not as fortunate as we are. Forget financial awareness, they are not able to understand the English language as well. How do you expect them to be more empowered?

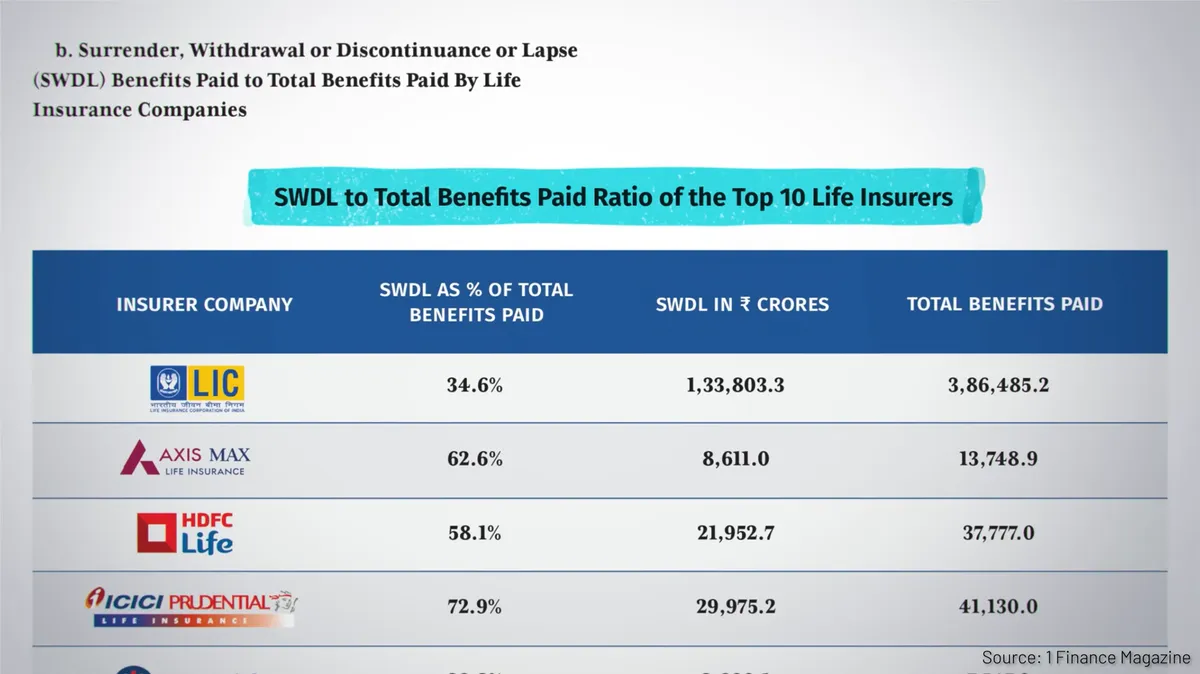

I believe awareness spreads best with network effects. If you are in the vicinity of someone who is not tech-savvy enough, and is looking for advice, do not hesitate to chip in. The malpractice of fraudulently selling the policies have now become a systemic issue and needs deep-rooted change. This of course can start if the IRDAI bars number-based incentives and rather introduces dropoff-rate based incentive structure. The drop-off rates indicate how many policyholders exit the scheme, often before maturity and at high exit costs. On average, 50% of policies are terminated within a five-year period since inception, highlighting the issue. A snip from the Mis-Sold documentary provides the drop-off rates for leading insurers.

Let's hope for a better tomorrow, and utilize AI as a companion in this journey to expose the farce that happens today at scale.